Types Of Tax Deductions

Published:

Key Takeaways

- Standard vs. Itemized Deductions: As a taxpayer, you can choose between the standard deduction (a fixed amount based on filing status) or itemized deductions (individual expenses). Either will always be the better option with greater tax benefits for someone.

- Keep Detailed Records: In case you want to claim itemized deductions, keep receipts, invoices, and other documentation to back your claims in case of an audit.

- Know Deduction Limits: Some deductions, like medical expenses, are subject to income thresholds, meaning only expenses exceeding a certain percentage of your adjusted gross income (AGI) are deductible. Avoid nasty surprises by keeping these thresholds in mind if you plan to itemize deductions.

- Use IRS Forms Correctly: Itemized deductions are reported on Schedule A (Form 1040). However, other specific deductions, such as student loan interest or educator expenses, are reported in specific lines on Form 1040.

- Stay Updated on Tax Law Changes: Tax laws change frequently (some of them yearly), which can affect deduction eligibility and amounts. Always check the latest IRS guidelines or consult a tax professional to ensure compliance and maximize deductions (or at least make sure that your tax professional is doing so).

An Overview of the Types of Tax Deductions & How to Claim Them on Your Return

With the ever-changing tax laws and the temporary nature of most tax credits and deductions, timing is critical when it comes to claiming anything on your income tax return. To make the most of the available benefits, taxpayers often choose to defer their income and accelerate their tax deductions.

Tax deductions lower your taxable income, and they are calculated using the percentage of your marginal tax bracket. For example, if you are in the 24% tax bracket, a $1,000 tax deduction saves you $240 in tax (0.25 x $1,000 = $250).

As you prepare your income tax return, you must decide between taking the standard deduction or itemizing deductions. You should use whichever tax deduction benefits you the most.

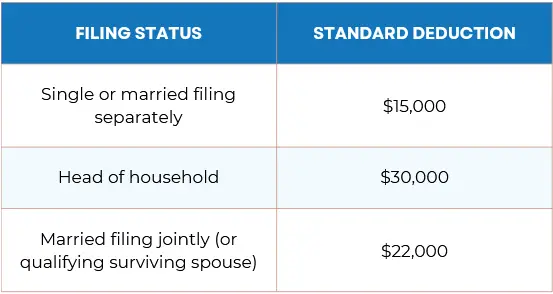

The Standard Deduction

The standard deduction is a dollar amount that reduces your taxable income. It is usually adjusted for inflation every year. Your standard deduction amount is based on your filing status, and it is subtracted from your AGI (adjusted gross income).

An additional standard deduction for the elderly (over 65) or visually impaired is as follows:

- $1,700 for single or head of household filers

- $1,350 for married filers

The standard deduction can be claimed on your individual income tax return (Form 1040).

RELATED: 2021 Federal Income Tax Rates, Brackets, & Standard Deductions

Itemized Deductions

If you do not qualify for the standard deduction, you may choose to itemize your deductions instead. A taxpayer will also typically itemize deductions if it offers them more benefits than the standard deduction (i.e., when the total amount of qualified deductible expenses is greater than the standard deduction).

Certain itemized deductions are based on a minimum (or “floor”) amount. This means that you can only deduct amounts that exceed the specified “floor.” However, there is no longer an income limit for taxpayers who itemize.

If you paid for any of the following items during the tax year, you may be able to use them to claim an itemized deduction:

- Medical and dental expenses

- Deductible taxes

- Home mortgage points

- Interest expenses

- Charitable contributions

- Business use of your home or car

- Business travel expenses

- Work-related education expenses

- Casualty, disaster, and theft losses

If you decide to itemize your deductions, it is important to keep detailed records of those tax deductions – including documentation for medical expenses, charitable donations, interest expenses, and business expenses. You should use IRS Tax Schedule A (Form 1040) to figure your itemized deductions, and file it with your 1040 tax return.

Here are links to the IRS tax forms for calculating and reporting your itemized deductions:

RELATED: The Standard Deduction vs. Itemized Deductions

Above-the-Line Deductions

Above-the-line tax deductions are taken before your AGI is calculated (instead of after, like the other deductions). Because of this, many believe this type of tax deduction to be more advantageous to taxpayers. Above-the-line deductions are subtracted from your gross income, and the resulting number is your AGI.

These tax deductions apply whether you itemize or not. They were designed to help protect your personal exemptions and itemized deductions from phase-outs.

Some above-the-line deductions include the following:

- Student loan interest

- Certain business expenses

- Alimony

- Half of self-employment tax

- Contributions to a qualified retirement account (e.g. traditional IRA)

- Contributions to a Health Savings Account (HSA)

- Early withdrawal penalties for CDs and savings accounts

- Moving expenses for members of the U.S. military

RELATED: How to Determine Your Income Tax Bracket

Types of Tax Deduction: FAQ

1. What is a tax deduction, and how does it differ from a tax credit?

Simply put, a tax deduction reduces your taxable income, which lowers the amount of income that is subject to taxes (not your tax liability which is how much you actually owe in taxes). For example, if you earn $50,000 and claim $5,000 in deductions, you’ll only pay taxes on $45,000.

In contrast, a tax credit directly reduces the amount of tax you owe. Say, if your tax bill is $3,000 and you claim a $500 tax credit, you’ll only owe $2,500. Remember this simple phrase: Deductions lower taxed money, while credits lower owed money.

2. What are the most common tax deductions available to individuals?

Too many to include in a single answer of this FAQ. If you want to know some of the most widely-used tax deductions, you’ll be looking at the following:

- Standard Deduction: A fixed amount based on your filing status (e.g., single, married filing jointly).

- Mortgage Interest Deduction: For homeowners paying interest on a qualified home loan.

- Charitable Contributions: Donations to eligible charities can often be deducted.

- State and Local Taxes (SALT): Includes property taxes and either income or sales tax, up to $10,000.

- Medical and Dental Expenses: Deductible if they exceed 7.5% of your adjusted gross income (AGI).

- Student Loan Interest: Up to $2,500 annually for interest paid on qualified loans.

3. Are there deductions specifically for self-employed individuals?

Yes, self-employed individuals have access to unique deductions, including home office deduction for those using a portion of their home exclusively for business; health insurance premiums that can be deducted for self-employed individuals; business expense costs such as office supplies, advertising, and travel; vehicle expenses like the standard mileage rate or actual costs if the vehicle is used for business; and the classic retirement contributions to SEP IRAs, SIMPLE IRAs, or solo 401(k) plans.

4. Can I deduct education-related expenses?

Absolutely yes, certain education-related expenses are deductible, such as:

- Tuition and Fees Deduction: For qualified higher education expenses (up to $4,000, if eligible).

- Lifetime Learning Credit (LLC): Technically a credit, but closely tied to education expenses for ongoing learning.

- Work-Related Education: Expenses for courses or certifications that improve skills in your current job.

These deductions and credits depend on income limits and other eligibility criteria.

5. What is the difference between itemized deductions and the standard deduction?

The standard deduction is a fixed amount you can subtract from your income based on your filing status. It simplifies tax filing and eliminates the need to list individual expenses.

Itemized deductions, on the other hand, allow you to list specific expenses (e.g., mortgage interest, medical costs) to potentially exceed the standard deduction. One is simple and saves you a not-so-terrible amount in taxes, while the other is more time-consuming and labor-intensive, but has the potential to save you a lot more on taxes when done right. Which one you choose is up to you and depends on your individual situation.

6. What are some overlooked deductions taxpayers often miss?

With millions of taxpayers in the US, you can bet there are some mistakes that get made more often than others, as well as deductions that could benefit lots of people but are simply ignored. Here are a few commonly overlooked deductions:

- Job Search Expenses: Costs related to searching for a new job in your current field (e.g., resume preparation, travel).

- Moving Expenses: If related to active-duty military service.

- Educator Expenses: Up to $300 for teachers purchasing classroom supplies.

- Energy-Efficient Home Improvements: Certain upgrades (e.g., solar panels, energy-efficient windows) may qualify.

- Casualty and Theft Losses: Losses due to federally declared disasters may be deductible.

7. How can I ensure I’m maximizing my tax deductions?

It’s in your best interest to know all the ins and outs of claiming deductions if you don’t want to leave money on the table every year with taxes. Here’s how to make the most of your available deductions:

- Keep Detailed Records: Maintain receipts, invoices, and financial statements for deductible expenses.

- Use Tax Software or a Professional: Tax preparation software or a CPA can help identify deductions you might miss.

- Stay Informed: Tax laws change frequently, so stay updated on new deductions or altered eligibility requirements.

- Plan Ahead: For instance, bunching charitable contributions into one year can help maximize itemized deductions.

If in doubt, consult a tax professional to ensure you’re taking advantage of every deduction applicable to your situation.

Related Articles

You May Also Like