How To Pay Taxes: The 6 Best Payment Options

Published:

Key Takeaways

- The IRS provides multiple ways for you to file and pay your taxes, from traditional mail to electronically, and even in person.

- Most payment methods are free, but some of them (such as paying with debit/credit card) have additional costs.

- There are options for those who cannot pay their taxes in full before the due date, such as installment plans, to avoid incurring in penalties.

- The IRS has an official, free app that allows you to pay your taxes through your mobile device.

- Offer In Compromise (OIC) is the option to get a reduced tax bill for those who have lost their jobs or had their business fail.

How To Pay Taxes: Everything You Should Know

Want to know how to pay taxes? Everyone has to pay taxes—that much is obvious. But you probably don’t know just how many options you have to do it. The IRS offers plenty of avenues on which to pay your tax bill, each with its own pros and cons which we will be explaining one by one.

The most well known are, of course, through the tax-prep programs that people use, but did you know that you can use Direct Pay, or even your credit card? And there’s always snail mail (though the IRS discourages this being your first option nowadays).

There Are Several Ways You Can Pay Down Your Taxes

In order to determine how much income tax you owe, you will first need to prepare your tax return. You have until April 15th to file and pay your individual income tax. If you miss the deadline, you will be charged penalties and interest.

>> Owe the IRS? Get a Free Tax Relief Consultation

The IRS gives you several options for paying your taxes. To pay your tax liability in full right away, use one of these methods:

1. Pay With a Bank Account (Direct Pay)

Let’s start things off with what is, perhaps, the easiest way to pay your Federal taxes: Using “Direct Pay” on the IRS.gov website. This method allows you to pay your tax bill directly from your checking or savings account. You will need to provide your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) to use the Direct Pay system. When making a tax payment, you will be asked the reason for your payment — make sure to select “Tax Return” so your payment is applied to the amount owed on your income tax return.

Pros Of Using Direct Pay For Your Taxes

- It’s a completely online method.

- You can schedule your payment up to a full year in advance.

- Same-day payments are an option, as is editing or canceling a scheduled payment (up until two days before the date).

- You get email notifications about the status of your payment.

Cons Of Using Direct Pay For Your Taxes

- You’re limited to two payments every 24 hours.

- Processing each payment can take up to two business days.

- If you’re living abroad, you can’t use an international bank account (unless it’s a U.S. bank affiliate).

2. Pay By Check or Money Order

If you are filing a paper tax return, you can make a payment by check or money order. Use IRS Form 1040-V (Payment Voucher) to submit your payment. Form 1040-V can be mailed to the IRS in the same envelope as your tax return — just don’t staple the forms together. Make sure you use the correct IRS mailing address for your tax payment.

Pros Of Paying Your Taxes By Check Or Money Order

- Money orders don’t require you to have a bank account.

- Money orders and cashier’s checks can’t bounce, so your payment is more secure.

- It’s possible to get a cashier’s check without a bank account (make sure to check first).

Cons Of Paying Your Taxes By Check Or Money Order

- Money orders are usually limited to $1,000.

- They have to be mailed physically.

- Regular checks can bounce.

- Requires you to move around more than other options.

3. Pay With Cash

If you want to pay your taxes in cash, the IRS provides a way for you to do this at participating retail stores. The program is called “PayNearMe” and there’s a $3.99 fee per cash payment. Note that it usually takes 5-7 business days to process cash payments, so make sure you know the applicable tax deadline and plan ahead to ensure that your payment is received on time.

In some cases, you might not have enough money in your bank account to fully pay your tax bill by the due date. The IRS gives you several options here – although you should always pay as much as you can by the deadline in order to minimize penalties and interest.

Pros Of Paying Your Taxes Using Cash

- Zero need for a bank account.

- Could be more convenient for some types of employees.

- The IRS is partnered with many U.S. retailers, such as Walmart, CVS, Walgreens, 7-Eleven, and Family Dollar.

Cons Of Paying Your Taxes Using Cash

- Some IRS offices require you to make an appointment 30 to 60 days in advance.

- Limited to $500 per payment.

- Requires you to move around carrying large amounts of cash, which can be possibly dangerous.

- Time consuming.

4. Pay By Debit or Credit Card

If you don’t have enough funds in the bank, but you do have available credit on a credit card, you may use your credit card to pay your taxes. Visit the IRS website for a list of Payment Processors. Keep in mind that there is a processing fee for using your credit card (the fees are listed and vary by service provider). Most of the time, the interest/fees associated with paying your taxes by credit card are less than the interest and penalties imposed by the IRS for paying late, making this a viable option for many people who don’t have the cash on-hand.

Pros Of Paying Taxes Using Debit Or Credit Card

- Can be done either online or through the phone with the help of an IRS employee.

- A plethora of accepted options, such as Visa, Mastercard, American Express, Cirrus, Discover, and digital wallets like Venmo and PayPal.

Cons Of Paying Taxes Using Debit Or Credit Card

- Processing fees are applied for both debit and credit card payments, which increase according to the payment amount.

- At least part of your tax information will go through a third party.

- If using a credit card, paying high amounts can negatively impact your credit score.

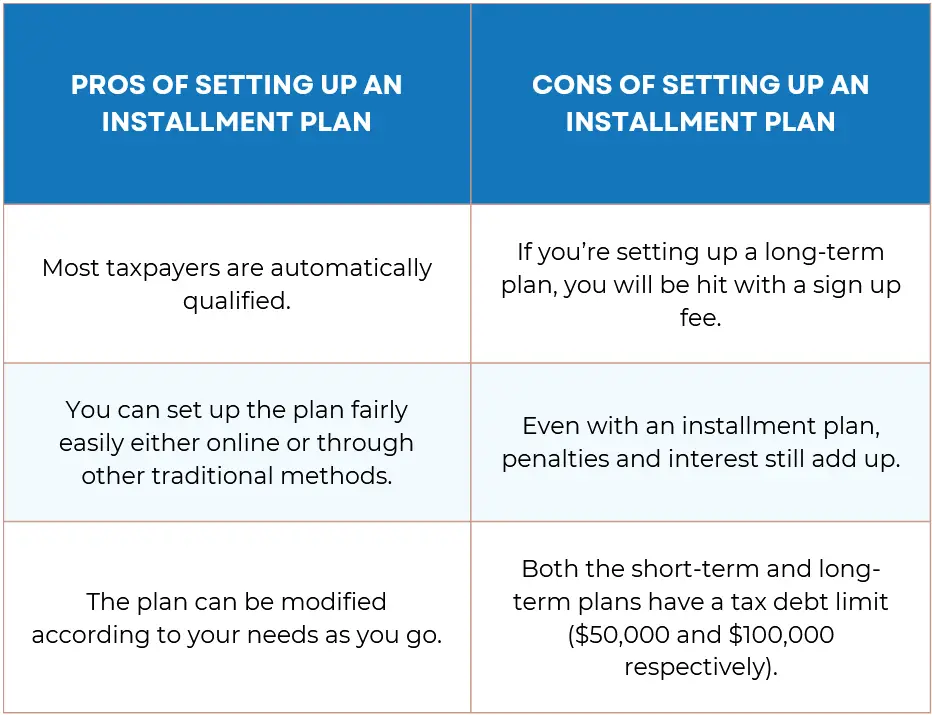

5. Set Up a Payment Plan (Installment Plan)

If you owe $50,000 or less in taxes, you can apply for an Online Payment Agreement on the IRS website. This means you would agree to pay your tax balance in installments over time. Note that interest will still accrue on your unpaid balance, however, you will not be considered in default. To apply, you’ll need to provide the IRS with information about your income and tax liability. In many cases, they will be able to give you a decision immediately online.

6. Offer to Settle

If it will cause “extraordinary hardship” to pay your tax liability, you can make a settlement offer to the IRS. This is called an Offer in Compromise. Essentially, you offer to pay a portion of your taxes immediately and the IRS agrees to drop the rest. There’s a lot of paperwork to fill out in order for a settlement to be approved, and you’ll need to demonstrate that it’s impossible for you to fully pay the taxes that you owe. If you are able to pay your taxes through an installment plan, you will not be eligible for an Offer in Compromise.

Pros Of Requesting An Offer In Compromise

- Can really make a difference for people in dire financial straits due to external factors.

Cons Of Requesting An Offer In Compromise

- For the IRS to consider your application, you must have filed your taxes for the year and be current on all payments from previous years.

- Taxpayers that are currently involved in bankruptcy proceedings cannot apply for an OIC, so it might make things harder if you’re already in a bad position.

- You have to pay a fee to set up the OIC, although the IRS can lower/eliminate it if you qualify for the Low-Income Certification.

What Happens If You Don’t Pay the IRS?

If you do not pay your taxes by the due date, the IRS will begin the collection process. Interest compounds daily and monthly penalties will be assessed on your unpaid balance.

Neglecting to pay your taxes can result in a Federal tax lien from the IRS. A tax lien is a claim on your property for failing to pay taxes. A tax lien allows the IRS to garnish your wages and other assets. Furthermore, a lien will not be lifted until the taxes and penalties are paid in full.

How To Pay Taxes: FAQ

1. What are the different ways to pay taxes?

There are several ways you can pay your taxes, such as the ones described below. Remember to check all the necessary details for each method.

- Online: Taxpayers can use the IRS website to pay their taxes through Direct Pay, the Electronic Federal Tax Payment System (EFTPS), or with a debit/credit card.

- Mail: You can send a money order or check for the total amount of your tax liability to the IRS to the appropriate IRS address using regular mail.

- Bank account: You can use your bank account to schedule your tax payment when e-filing your return.

- In person: You can go directly to your local IRS office (or even participating retail partners) to pay your taxes. Remember to bring all your documentation with you.

2. Do I have to pay my taxes in full every time?

No. If you, for any reason, are unable to pay your tax liability in full, you can apply for a short-term or long-term payment plan from the IRS (depending on how much you owe). You might need to pay a setup fee if you choose the long-term plan, but some low-income taxpayers can ask for a reduced rate.

3. What information do I need to provide to pay my taxes?

The specific documentation you need depends on your specific case, but as for personal documentation you will need:

- Social Security Number (SSN) or Taxpayer Identification Number (TIN).

- Bank account details, or payment details if paying electronically.

- All applicable tax forms, such as W-2s for each employer you have.

- Your total gross income, AGI, and MAGI.

4. What if I can’t pay my taxes in full by the deadline?

First thing you’ll want to do if you can’t pay the full amount you owe is to pay as much as you can; this way you will reduce penalties and interest on your tax debt. Next, you definitely want to contact the IRS to set up a payment plan as soon as possible, whether it’s a short-term or long-term plan.

5. Will the IRS notify me if they received my payment?

It depends on what payment method you chose. The IRS will send a confirmation number if you paid electronically to the address you provided in your return. If you mailed your payment, you can ask your carrier for proof of delivery. Also, you can verify if your payment has been processed through your online IRS account.

6. Does the IRS charge any fees for paying with credit or debit card?

No. The IRS doesn’t charge any fees for debit or credit card payments, but your bank may charge processing fees for doing so. These processing charges are not considered part of your payment because they are not collected by them.

Related Articles

You May Also Like