When you hear cryptocurrency, your mind may automatically jump to big names like Bitcoin and Ethereum. What you may not think of is taxes. However, like other assets, cryptocurrency (and virtual currency broadly) is taxed.

Here are some helpful FAQs to help you understand how the IRS treats virtual currency, crypto, and other digital currency initiatives.

What is cryptocurrency (according to the IRS)?

Virtual currency is a digital representation of value (other than a representation of the U.S. dollar or a foreign currency, a.k.a. “real currency”) that functions as a unit of account, a store of value, and a medium of exchange. The IRS uses the term “virtual currency” to describe the various types of convertible virtual currency – including digital currency and cryptocurrency. Cryptocurrency is a type of virtual currency that uses cryptography to secure transactions that are digitally recorded on a distributed ledger, such as a blockchain.

Some virtual currencies are convertible, which means that they have an equivalent value in real currency or act as a substitute for real currency. Bitcoin is one example of a convertible virtual currency. Bitcoin can be digitally traded between users and can be purchased for, or exchanged into, U.S. dollars, Euros, and other real or virtual currencies.

Do I Have to Tell the IRS If I bought cryptocurrency?

Form 1040, the individual tax return form, asks whether, at any time during the year, you received, sold, sent, exchanged, or otherwise acquired any financial interest in any virtual currency. If you purchased cryptocurrency with real currency (e.g., U.S. dollars) but had no other transactions during the year, you are not required to answer “yes” to the Form 1040 question, and you do not owe taxes on it.

How is cryptocurrency taxed?

Cryptocurrency and other virtual currencies are treated like property for tax purposes. So the general rules that apply to other kinds of property in which people commonly invest (like stocks and gold) also apply to crypto. (For more information on the tax treatment of property transactions, see IRS Publication 544 (Sales and Other Dispositions of Assets)).

As noted, just buying crypto doesn’t mean that you’ll be taxed. Taxation starts happening whenever you use crypto as a “method of exchange”, or a means of buying other things. It is also taxable when you receive cryptocurrency as a form of income.

Taxable events include:

exchanging your convertible virtual currency (like Bitcoin) for U.S. dollars

using virtual currency to pay for goods and services

exchanging your virtual currency for another virtual currency

getting paid in crypto for a good or service provided

Crypto mining

Receiving air dropped tokens (or receiving several tokens of a new cryptocurrency for free at its launch)

Staking cryptocurrency (this refers to rewards earned for holding cryptocurrency for longer periods, not unlike the interest you receive on a savings account)

Cryptocurrency tax rate

Different cryptocurrency transactions have different tax rates. The applicable rate depends on whether you are on the buying end or the receiving end of a cryptocurrency transaction. Capital gains tax applies if you are ‘disposing’ of your cryptocurrency (selling or exchanging it), while income tax applies if you are receiving crypto as payment or from mining, staking, or airdropping. The sections below provide more details about different crypto tax rates.

Crypto and capital gains tax

When you sell virtual currency, use it to pay for a good or service, or exchange it for another virtual currency, you are ‘disposing’ of your cryptocurrency investment. This ‘disposal’ will result in a capital gain or loss, depending on whether the value of the virtual currency has increased or decreased since you bought it. As with other investments, these capital gains and losses are taxed under the capital gains tax.

There are two different tax rates depending on how long you’ve held your cryptocurrency:

Short-term capital gains tax applies if you had had your crypto for a year or less when you sold it. The short-term capital gains tax rates are the same as you pay on other forms of income: they range from 10% to 37%, depending on your income tax bracket and filing status.

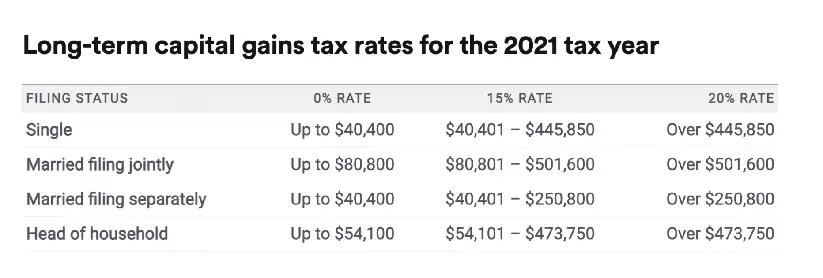

Long-term capital gains tax applies if you’ve had your crypto for a year or more. The long-term capital gains tax rate is lower than the short-term capital gains tax rate. It ranges from 0% to 10%, depending on your tax bracket and filing status.

How to calculate capital gains and losses

To calculate your capital gain or loss, you must first know the ‘cost basis’ of your cryptocurrency. This is essentially the fair-market value (in U.S. dollars) of the crypto when you first bought it. Your gain or loss will be the difference between the cost basis and the amount you received in exchange for the virtual currency. This will need to be reported as U.S. dollars on your federal income taxes.

For example, let’s say you are a single person who bought $1,000 worth of a certain cryptocurrency a few years back. This year, the price exploded, and now the fair market value of your crypto is $20,000. You used the money to buy a new car. In doing so, you are disposing of your asset and making a gain of $19,000.

To calculate the tax you owe, you first need to subtract the original cost basis from the $20,000. This gets you $19,000. Because you had had the cryptocurrency for several years at this point, you would be taxed at the long-term capital gains tax rates in the table above.

If someone pays you for a good or service using cryptocurrency, the payment is taxed as taxable income, just like cash. When filing your taxes, you will need to report the fair market value of the cryptocurrency at the time you received it, in U.S. dollars (the cost basis of the crypto).

Taxing crypto mining

Cryptocurrency mining refers to the use of special, highly complicated computer algorithms to verify transactions involving that currency and add them to the blockchain. Miners are compensated for this work in cryptocurrency. This compensation is considered a form of taxable income. And, as with being paid in cryptocurrency, you need to report this income in terms of the fair market value at the time you received it.

How you report the income you earned from mining depends on whether you mine as a hobby or a business. If you’re running a crypto mining business, then you will need to file a Form 1099-NEC , which allows you to disclose self-employed income. If mining is a hobby, then you will report it on line 8 of your form 1040 (other income).

Taxing crypto staking and air dropping

As with mining, you will need to report any income you earn by staking cryptocurrency or receiving airdropped tokens on line 8 of your 1040 (“other income”).

What happens if you don’t report cryptocurrency on taxes

Given how much of a headache it can be to file taxes for your cryptocurrency gains, you may be wondering what happens if you don’t file.

In short, if you fail to report taxable income related to cryptocurrency and get audited, things could get ugly. At the very least, you will have to pay interest on the amount you owe. But beyond that, you could face penalties or even criminal charges of perjury (lying under oath), tax evasion, or fraud.

The best course of action is to keep good records, start your taxes early, and be truthful. You may want to get professional services to help you make sure your tax bill is audit-ready.

What records do I need to maintain for virtual currency transactions?

The Internal Revenue Code and regulations require that you maintain records that sufficiently verify any claims you make on your tax returns. To do this, you’ll need to maintain records documenting receipts, sales, exchanges, or other dispositions of virtual currency and the fair market value of the virtual currency.

For U.S. tax purposes, transactions using virtual currency must be reported in U.S. dollars. This means you must determine the fair market value of virtual currency in U.S. dollars as of the date of payment or receipt. If a virtual currency is listed on an exchange and the exchange rate is established by market supply and demand, the fair market value of the virtual currency is determined by converting the virtual currency into U.S. dollars (or into another real currency which in turn can be converted into U.S. dollars) at the exchange rate, in a reasonable manner that is consistently applied.

Nick Charveron

Nick Charveron is a licensed tax practitioner and Partner & Co-Founder of Community Tax, LLC. As an Enrolled Agent, the highest tax credential issued by the U.S. Department of Treasury, Nick has unrestricted practice rights before the IRS. He earned his Bachelor of Science from Southern Illinois University while serving with the U.S. Army Illinois National Guard and interning at the U.S. Embassy in Warsaw, Poland. Based in Chicago, Nick combines his passion for finance and real estate with expertise in tax and accounting to help clients navigate complex financial challenges.