The Child Tax Credit

Published:

A Tax Break for People Who Have a Qualifying Child

One of the most valuable and popular federal tax credits is the Child Tax Credit.

For tax year 2019, the Child Tax Credit (CTC) is worth up to $2,000 per qualifying child. Furthermore, up to $1,400 of that amount can be refundable. A refundable tax credit can reduce your tax liability beyond zero and result in a tax refund for you.

What Is a Qualifying Child?

You may be eligible for the Child Tax Credit if you have a qualifying child under age 17 and you meet other IRS requirements. The maximum amount allowed for this tax credit is $2,000 for each qualifying child.

If you want to claim the Child Tax Credit, your qualifying child must have a Social Security Number (SSN) that was issued by the Social Security Administration before the due date of your income tax return. This requirement is also true for the Additional Child Tax Credit (see below). Children with an ITIN (Individual Taxpayer Identification Number) cannot be claimed for either child tax credit.

In general, a person is considered your “qualifying child” for the purposes of this tax credit if all of the following apply:

- The child is closely related to you (e.g., your son, daughter, stepchild, eligible foster child, brother, sister, stepbrother, stepsister, half brother, half sister, grandchild, nephew, or niece)

- The child was under age 17 at the end of 2019

- The child is claimed as a dependent on your tax return

- The child did not provide more than half of his/her own support during 2019

- The child does not file a joint tax return for the year, or files a joint return only to claim a tax refund for withheld income taxor estimated tax paid

- The child lived with you for over half of 2019

- The child is a U.S. citizen, U.S. national, or U.S. resident alien

For a full list of requirements, see IRS Publication 972 (Child Tax Credit and Credit for Other Dependents).

You can use the IRS online tool to see if you’re able to claim this tax break: Does My Child/Dependent Qualify for the Child Tax Credit?

Are There Income Limits for the Child Tax Credit?

For tax year 2019, the maximum credit is $2,000 per qualifying child. There are some limits to how much you can claim for the Child Tax Credit if your income is above a certain level, based on your filing status. The credit begins to phase out at $400,000 of modified adjusted gross income for married couples filing jointly, and $200,000 for all other filing statuses.

How Do I Claim the Child Tax Credit?

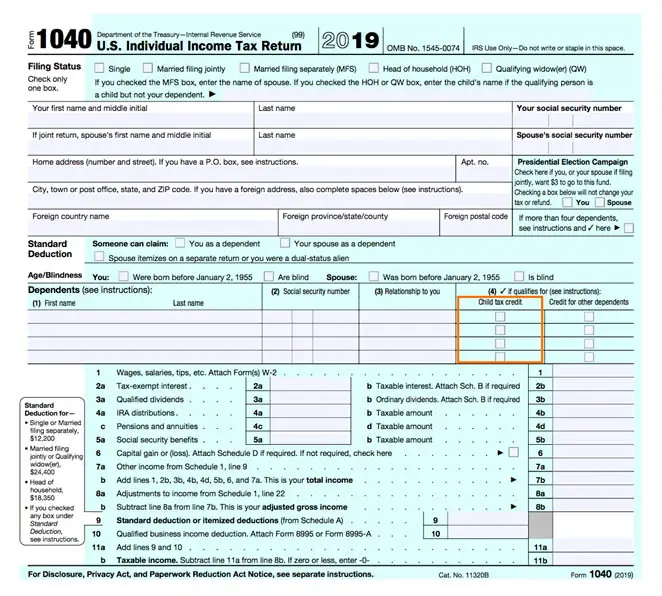

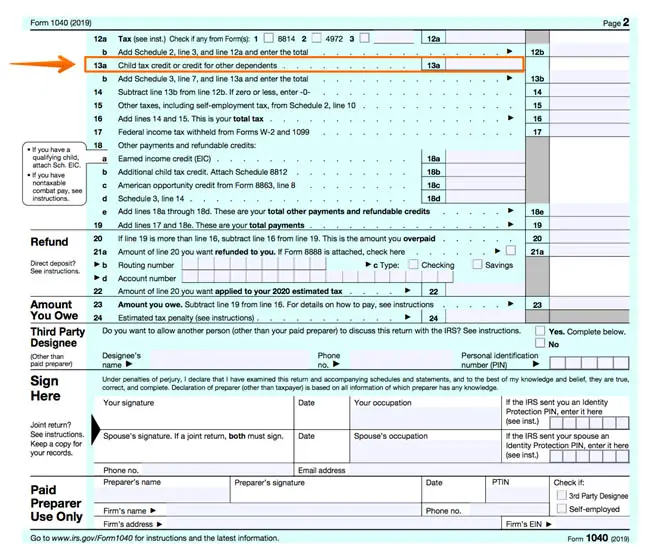

There are currently two sections where you report information about your qualifying child (a.k.a. dependent) and claim the Child Tax Credit – the front and the back of Form 1040.

On the front of Form 1040, you enter information about your dependents. If your dependent qualifies for the Child Tax Credit, you should check the corresponding box:

On the back of Form 1040, you enter the amount you are claiming for the Child Tax Credit on Line 13a:

For detailed line-by-line guidance, see the Instructions for IRS Form 1040.

What About the Additional Child Tax Credit?

The Additional Child Tax Credit (ACTC) is for certain individuals who receive less than the full amount of the Child Tax Credit (CTC). The ACTC is a refundable tax credit, which means it can reduce your tax liability below zero and result in a tax refund. Beginning with tax year 2018, the Additional Child Tax Credit is no longer a separate credit from the Child Tax Credit.

Similar to the Child Tax Credit, the Additional Child Tax Credit also now requires your qualifying child to have a Social Security Number (SSN) that was issued by the Social Security Administration before the due date of your income tax return. This means that children who have an ITIN (Individual Taxpayer Identification Number) do not qualify for this tax credit.

The Additional Child Tax Credit is worth up to $1,400 and is available to taxpayers with more than $2,500 of taxable earned income who have at least one qualifying child.

You should use IRS Schedule 8812 (Form 1040) to calculate and claim the Additional Child Tax Credit.

Tax Credit for Other Dependents

If you have a dependent person who doesn’t qualify for the Child Tax Credit, he/she may still qualify you for the new Credit for Other Dependents (a.k.a. ODC). This non-refundable tax credit is worth up to $500 for each qualifying dependent (other than children who can be claimed for the Child Tax Credit). To be eligible for this credit, the dependent must be a U.S. citizen, U.S. national, or U.S. resident alien.

The Credit for Other Dependents is calculated and reported with the Child Tax Credit on your Form 1040. Note that there is a phaseout limit if your adjusted gross income (AGI) exceeds $400,000 for married taxpayers filing jointly – or $200,000 for all other filing statuses.

For more information, see IRS Publication 972 (Child Tax Credit and Credit for Other Dependents).

Related Articles

You May Also Like