Key Takeaways

- Your adjusted gross income (AGI) and modified adjusted gross income (MAGI) both represent your total income after a few subtractions or additions are made.

- AGI is usually a reduced version of your taxable income after certain deductions are made.

- MAGI is your AGI after further subtractions or additions, such as IRA contributions, self-employment tax, and others.

- Both AGI and MAGI are used by the IRS to determine whether you qualify for certain credits or additional deductions.

- Your MAGI is recognized by the IRS but does not appear on your tax return.

Adjusted Gross Income (AGI) and Modified Adjusted Gross Income (MAGI): When it comes to calculating your taxes, you will often hear those two different terms regarding income. You probably know that deductions are involved, and that one somehow follows the other (right?), but the details probably make you scratch your head by the end of the explanation.

Don’t worry, we’ll give you the ultimate breakdown for both AGI and MAGI so you’ll become a tax wiz in no time — or at least you’ll be able to figure out your tax forms a little better. Either way, don’t miss this guide!

What’s the Difference Between Your AGI and MAGI?

Both AGI and MAGI are important in determining your tax liability, as well as the amount of tax credits and tax deductions that can help lower your tax balance. Your AGI and MAGI will likely be close to each other in value. In many cases, a taxpayer’s AGI and MAGI are the same number, depending on what type of expenses they had during the year.

Understanding the difference between your AGI and MAGI will help you determine which tax rate(s) apply to you and what tax breaks are available to you.

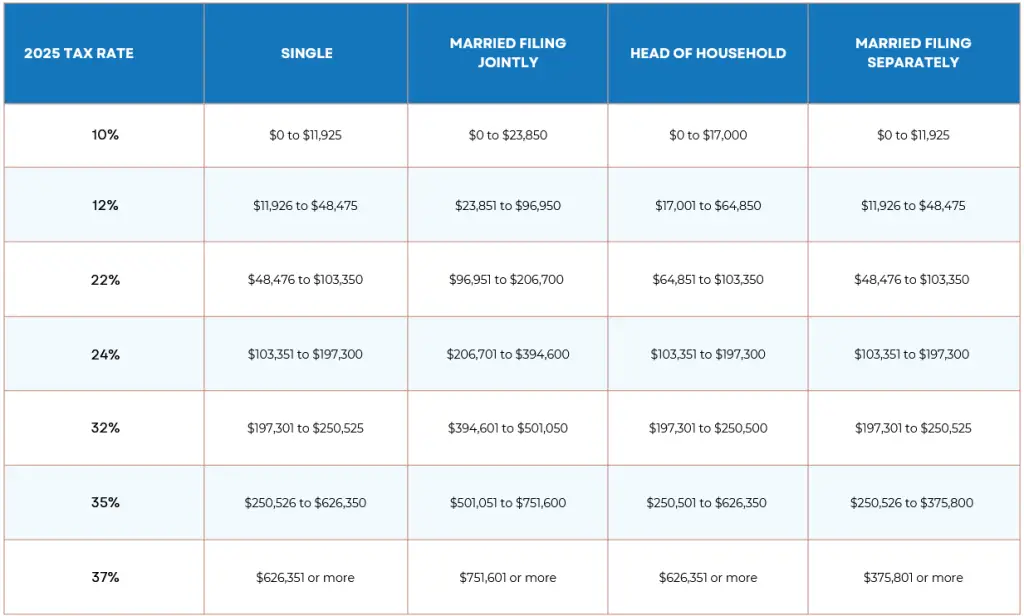

RELATED: 2019 Federal Tax Rates, Brackets, & Standard Deductions

Adjusted Gross Income (AGI)

Your AGI is the most commonly used income figure and can be defined as a modification of your gross income; that is, the total income you got in a tax year from any qualifying source. It generally includes all of the income you earn, minus certain adjustments. It’s used to determine your income bracket for tax purposes.

Not only that, but calculating your AGI is the starting point to determining whether you’ll be eligible for certain tax credits, deductions and other benefits.

Allowed Deductions On Your AGI

AGI refers to your total income for the year, minus certain adjustments that are allowed by the IRS. These adjustments are listed in the Instructions for Form 1040 and on Schedule 1 (Form 1040 or 1040-SR). They include items such as:

- Health Savings Account (HSA) Contributions: You can claim a tax deduction on your contributions to an HSA (as long as they’re not made by your employer)

- Retirement Contributions: Contributions to traditional IRAs and 401(k)s, along with a few other qualifying retirement accounts, can be deducted.

- Tuition And Other Educational Fees: Up to a certain limit, qualified education expenses can be deducted from your AGI.

- Self-Employment Taxes: Self-employed taxpayers can deduct a portion of their self-employment tax.

- Student Loan Interest: You can deduct up to $2,500 of paid interest on qualified student loans.

- Alimony Payments: If your divorce was finalized before 2019 and you pay alimony, those payments can be deducted.

- Moving Expenses: Active-duty military personnel can claim deductions on their unreimbursed moving expenses.

Once the allowed items are subtracted from your income, you arrive at your AGI.

Your AGI determines whether or not you qualify for certain tax credits, such as the Earned Income Credit. There are also various tax deductions that are dependent on your AGI — including your total itemized deductions, mortgage insurance premiums, and medical deduction allowances.

Example Calculation Of Adjusted Gross Income

Let’s say your total gross income for the 2024 tax year is $70,000. This amount includes your wages, bonus, and all other qualifying sources of income. All you have to do now is subtract every qualifying deduction; for this example, we’ll use traditional IRA contributions, Health Savings Account (HSA) contributions, and student loan interest.

- IRA contribution: $4,000

- HSA contribution: $2,500

- Student loan interest: $1,300

Your AGI will be calculated as follows:

- Add up qualifying deductions: $4,000 + $2,500 + $1,300 = $7,800

- Subtract your deductions from your gross income: $70,000 – $7,800 = $62,200

- Your Adjusted Gross Income is $62,200.

RELATED: Top 5 Tax Deductions for Individuals

Modified Adjusted Gross Income (MAGI)

Your MAGI differs from your AGI in that it may be higher, with certain adjustments added back. These adjustments may include items that were previously subtracted from your income to arrive at your AGI (see above section). For most taxpayers, their MAGI is equal their AGI before subtracting any deduction for student loan interest.

Items Added To Your MAGI After Calculating Your AGI

Some items that can increase your MAGI may include the following:

- Foreign Earned Income: All foreign earned income must be added back to the MAGI if you excluded it from your AGI.

- IRA Contributions: After subtracting your contributions to traditional IRAs to calculate your AGI, you must add them back to your MAGI.

- Tax-Exempt Interest: All interest from tax-exempt bonds factor into your MAGI.

- Student Loan Interest: You guessed it, your student loan interest comes back for your MAGI after being deducted from your AGI.

- Rental Losses: This one is more context-dependent than other factors, but in general they are also added back to your MAGI.

Like your AGI, your MAGI can determine whether you qualify for certain tax benefits. One of the most popular is the ability to deduct your IRA contributions on your tax return. However, you may not qualify for that deduction if your MAGI is above a certain level.

RELATED: Taxable Income vs. Non-Taxable Income

Calculating Your MAGI

To make things easier, let’s begin with the AGI we calculated in the last example: $62,200. To calculate your MAGI, you need to add all eligible items outlined by the IRS, some of which were originally deducted from your gross income to calculate your AGI.

For this example, let’s use the following items:

- IRA contribution (added back): $4,000

- Student loan interest (added back): $1,300

- Foreign earned income: $2,800

- Tax-exempt interest: $1,100

Your MAGI will be calculated as follows:

- Add up all items: $4,000 + $1,300 + $2,800 + $1,100 = $9,200

- Add your the total sum of your qualifying items to your AGI: $62,200 – $9,200 = $71,400

- Your Modified Adjusted Gross Income is $71,400.

Why Is It Important To Know The Difference Between AGI and MAGI?

Now that you know that calculating your AGI and MAGI is not as hard as you thought, you should understand why both of them are of vital importance when doing your tax return. AGI is not only the bedrock of your taxable income (which directly affects your overall tax liability), it also determines if you’re eligible for multiple tax deductions and credits.

On the other hand (and equally important), your MAGI is used by the IRS to determine if you qualify for several tax benefits and a few government programs that cannot be determined by your AGI alone. If you plan to apply for these benefits, knowing your MAGI beforehand can save you time and a lot of frustration.

Getting the help of a professional when calculating either (or both) of them can go a long way to avoid costly mistakes and get as many tax savings as possible.

The Final Word on AGI vs. MAGI…

If you hire a tax professional to prepare your tax return, they can calculate your AGI and MAGI for you. They can also discuss how both of these amounts affect the tax credits and deductions you are eligible for. Most tax preparation software programs will also calculate those numbers for you.

If you are preparing your own tax return, you will need to research which tax breaks are affected by AGI and MAGI so you can determine the amount of your tax savings.

RELATED: Who Has to File a Federal Income Tax Return?

Adjusted Gross Income (AGI) vs. Modified Adjusted Gross Income (MAGI): Frequently Asked Questions

1. What is Adjusted Gross Income (AGI)?

The AGI, as defined by the IRS, is your total gross income for the year minus certain allowed deductions. The resulting amount represents your taxable income before you make any itemized or standard deductions.

2. What is Modified Adjusted Gross Income (MAGI)?

After calculating your AGI, your MAGI “adds back” certain tax exemptions or deductions, but also tax penalties. The IRS uses your MAGI to check if you’re qualified to claim benefits such as student loan interest reductions or the Child Tax Credit.

3. What is the importance of MAGI?

The IRS will take your MAGI into consideration for determining your eligibility for various tax benefits and programs, such as:

- Roth IRA Contributions.

- Premium tax credits under the ACA.

- Deductions for student loan interest, as mentioned before.

- Any means-tested benefits, such as the Child Tax Credit.

4. Which is more important — AGI or MAGI?

Both your AGI and MAGI are important since both are used by the IRS to determine basic aspects of your tax return. The AGI determines your overall taxable income, which directly affects your tax liability for that year. On the other hand, you will need your MAGI to prove you qualify for specific credits and benefit programs.

5. How can I reduce my AGI?

There are a couple of ways to reduce your AGI with some common deductions, such as:

- Contribute to a Health Savings Account (HSA).

- Contribute to a traditional IRA.

- Contribute to your spouse’s IRA.

- Apply for all credits and deductions you qualify for.

- If you are self-employed, your health insurance premiums are deductible.

- While not the biggest money saver out there, student loan interests are also deductible.

Jacob Dayan

Entrepreneur • CEO Community Tax, LLC

Jacob Dayan is the CEO and co-founder of Community Tax LLC, a leading tax resolution company known for its exceptional customer service and industry recognition. With a Bachelor’s degree in Business Administration from the University of Michigan’s Ross School of Business, Jacob began his career as a financial analyst and trader at Bear Stearns and Millennium Partners before transitioning to entrepreneurship. Since 2010, he has led Community Tax, assembling a team of skilled attorneys, CPAs, and enrolled agents to assist individuals and businesses with tax resolution, preparation, bookkeeping, and accounting. A licensed attorney in Illinois and Magna Cum Laude graduate of Mitchell Hamline School of Law, Jacob is dedicated to helping clients navigate complex financial and legal challenges.