Form 982 helps you avoid paying taxes on certain types of canceled debt, like mortgage forgiveness, if you meet the qualifications for exclusion.

If you had debt wiped out in a bankruptcy or were considered insolvent at the time of cancellation, you might be able to use Form 982 to keep that forgiven debt from being taxed.

You usually need to receive a Form 1099-C before you even consider using Form 982. That 1099-C tells the IRS that a lender canceled your debt and that it could be treated as income unless you file this form.

Form 982 isn't just a one-and-done form. It sometimes affects your future tax benefits, especially if you have to reduce things like loss carryovers or depreciation, so the impact might show up in future years too.

Even though Form 982 is only one page long, it's full of complex terms and categories. It’s totally normal to get help with it—especially when it comes to calculating insolvency or understanding tax attribute reductions.

¿Le han cancelado o condonado alguna deuda este año? Es posible que necesite el Formulario de impuestos 982 del IRS..

Reclamar la insolvencia con el Formulario 982 puede permitirle excluir las deudas de sus ingresos gravables porque, sí, cuando no tiene que pagar una deuda, el gobierno federal llama a eso ingresos.

A menos que siga la guía paso a paso del profesional fiscal y planificador financiero certificado Forrest Baumhover de ¡Enséñame! Finanzas Personales. Como planificador financiero, Forrest ha ayudado a clientes a navegar por situaciones fiscales complejas durante años, y sus artículos sobre temas fiscales ayudan a cientos más.

Así que, si recibió un Formulario 1099-C durante el año, vea las instrucciones paso a paso de este planificador financiero para el Formulario 982, de modo que la deuda condonada no cuente como ingreso gravable en su próxima declaración de impuestos federales.

What is Form 982?

If you’ve recently had a debt forgiven or canceled, you might be surprised to learn that the IRS often considers that canceled amount as taxable income. That’s where Form 982 comes into play. This form is all about helping you reduce or eliminate that surprise tax bill if you qualify under certain rules. While it’s not something every taxpayer will need, if you’ve had a mortgage debt canceled, gone through bankruptcy, or had a lender write off a loan, then Form 982 might be very important for you.

You don’t need to be a tax pro to understand the basics, and knowing when and how to use Form 982 can potentially save you from a major tax hit. OK, so let’s walk through the key points first so you can get a clearer picture of what this form is, how it works, and how it might apply to your situation.

What Form 982 Actually Does

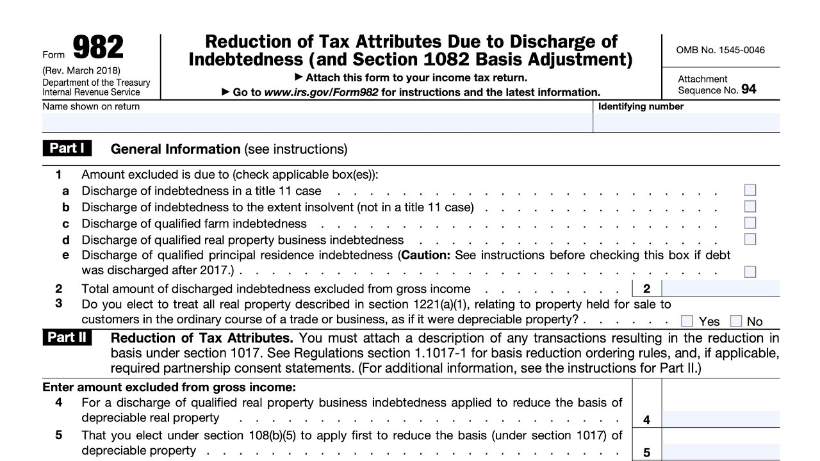

Form 982, officially called “Reduction of Tax Attributes Due to Discharge of Indebtedness,” is used to tell the IRS why certain canceled debt shouldn’t be treated as taxable income. In simple terms, this form is your way of saying, “I know a debt was canceled, but here’s why I shouldn’t have to pay taxes on it.”

The IRS generally treats canceled debt as income, meaning you’d have to report it and potentially pay taxes on it. That can be a harsh surprise, especially if you’re not in a great financial position to begin with. But there are exceptions, and Form 982 is how you claim those exceptions. Some of the most common situations where this form comes into play include bankruptcy, insolvency (where your total debts are greater than your assets), or certain types of mortgage debt cancellation.

Who Should Use Form 982?

If your lender sent you a Form 1099-C, which reports canceled debt to both you and the IRS, don’t panic just yet. You should first determine if you qualify for one of the exclusions allowed under the tax code, which would let you avoid reporting that amount as income. The most common reasons for using Form 982 include the discharge of debt during a bankruptcy, or when you were considered insolvent at the time the debt was forgiven.

Mortgage debt is another big one. If you lost a home or went through a short sale or loan modification, there’s a good chance some of the forgiven balance was reported to the IRS. Under the current tax laws, the exclusion for qualified principal residence indebtedness has been extended through at least 2025. If your main home was involved and the canceled amount meets the criteria, you can use Form 982 to exclude it from your taxable income.

The Role of Insolvency and Bankruptcy

Two of the main exclusions that allow you to file Form 982 are insolvency and bankruptcy. Insolvency simply means that your total debts exceeded your total assets at the time the debt was canceled. If that was the case for you, you may be eligible to exclude some or even all of the canceled debt. But it’s not automatic. You’ll need to figure out your total assets and liabilities at that point in time and compare them.

Bankruptcy works a little differently. If your debt was discharged as part of a bankruptcy proceeding under Title 11, then you almost always qualify to exclude that canceled amount using Form 982. However, to use this exclusion, the cancellation must be directly tied to your bankruptcy case, and you need to file the form the same year the discharge occurred.

How to Fill Out Form 982

The form itself is only one page long, but it’s loaded with technical language and options. The most important part is Part I, where you check a box to show which reason you’re using to exclude the income. You’ll also report the total amount of discharged debt that qualifies for the exclusion.

In Part II, you may need to reduce certain “tax attributes.” This is a fancy way of saying that while the IRS might let you skip the income this year, they’ll want to reduce some of your future tax benefits, like carryover losses or depreciation on assets. If you’re not sure how that works or whether it even applies to you, this is a good time to ask for help from a tax preparer or accountant.

How Form 982 Connects to Your Other Tax Documents

If you received a 1099-C from a lender, it’s crucial to review it carefully and not just ignore it. That form tells the IRS you had canceled debt. If you qualify for an exclusion but don’t file Form 982, the IRS could treat that amount as regular income—and that could inflate your tax bill by hundreds or even thousands of dollars.

Form 982 doesn’t work in a vacuum. It needs to be included with your federal tax return, along with any supporting documentation related to your debt situation. If you were insolvent, you might need to do a separate worksheet showing your assets and debts at the time. If you went through bankruptcy, you may need to show your discharge paperwork. This form is a tool, not a magic fix, and using it correctly is key.

When Not to Use Form 982

It’s also important to know when this form doesn’t apply. If your debt was canceled as a gift, if it was business debt that qualifies under a different exclusion, or if it was student loan debt discharged due to death or permanent disability (which isn’t considered taxable in most cases now), then Form 982 may not be the right fit.

Some types of forgiven debt also don’t need to be reported at all, such as certain Paycheck Protection Program (PPP) loans or specific types of employer-related student loan repayment programs. So if your situation involves one of those, you likely don’t need to file Form 982 at all.

The Final Word on Form 982…

Canceled debt is never fun to deal with, and when the IRS steps in, it can feel even more overwhelming. But Form 982 exists to help taxpayers like you avoid being unfairly taxed on debt you couldn’t afford to pay back. Whether it’s from a tough financial year, a bankruptcy, or a housing crisis, this form could save you from a large and unexpected tax bill.

The key is to know what counts, understand how the form works, and be honest and accurate when filling it out. If you’re unsure about whether you qualify, it’s worth getting some professional advice. But don’t ignore the situation altogether—especially if you’ve received a 1099-C. Form 982 might just be the paperwork you didn’t know you needed.

1. What exactly is Form 982 used for? Form 982 is used to tell the IRS that you qualify for an exception that allows you to exclude certain canceled debts from being counted as taxable income. Normally, when a debt gets canceled or forgiven, the IRS treats that amount like money you earned. But if you meet certain criteria—like going through bankruptcy or being insolvent at the time the debt was forgiven—you may not have to pay taxes on it. This form is how you claim that benefit.

2. How do I know if I qualify to use Form 982? To qualify, your canceled debt must fall under one of several exceptions laid out in the tax code. The most common are discharge through bankruptcy, being insolvent when the debt was canceled, or having mortgage debt on your main home forgiven in certain situations. Insolvency means that at the time the debt was wiped out, your total debts were more than everything you owned. You’ll usually need to show some basic math to prove that. If you had a foreclosure, short sale, or loan modification on your primary home, that might also qualify under the mortgage exclusion rules, depending on the year and the circumstances.

3. What kinds of debt can be excluded using Form 982? Not all canceled debts qualify for exclusion. The ones that typically do include credit card debt forgiven while you were insolvent, mortgage debt on a principal residence forgiven under certain programs, and debts discharged during bankruptcy proceedings. On the other hand, if the cancellation was part of a business agreement, related to investment properties, or just a lender writing something off as uncollectible without your involvement, then it may still be taxable. Student loan debt that’s canceled due to death or disability usually isn’t taxable anymore either, but that falls under different rules and doesn’t require this form.

4. Do I need to include anything else when I file Form 982? Yes, Form 982 needs to be submitted with your regular federal tax return—not separately. You also might need to attach other documents, depending on your situation. For example, if you’re claiming insolvency, the IRS recommends doing a simple balance sheet to show your debts and assets at the time the debt was forgiven. If your exclusion is based on bankruptcy, the IRS might expect to see documentation that confirms your case and discharge. And if you’re excluding mortgage debt, you’ll likely need a 1099-C from your lender and any documents related to the property involved.

5. Can I file Form 982 by myself, or should I get help? It really depends on how complicated your situation is. If you’re confident reading IRS instructions and you’re only excluding a straightforward amount of mortgage debt, you might be fine filling it out on your own. But if your exclusion involves insolvency or bankruptcy, or if the forgiven debt amount is high, it’s smart to get help from a tax professional. Form 982 also has implications beyond just the current tax year. It can reduce your future tax benefits, so getting it right the first time really matters.

6. What happens if I don’t file Form 982 after getting a 1099-C? If you skip Form 982 and the IRS sees a 1099-C linked to your Social Security number, they’re going to assume that the full amount of the canceled debt is regular income. That can significantly increase your taxable income and potentially push you into a higher tax bracket, raising your tax bill by quite a bit. The IRS may also send you a notice asking for clarification or hit you with penalties and interest if they believe you underreported income. Filing Form 982 on time, with the right supporting info, is how you avoid that mess.

Markos Banos

Markos M. Baños Cabán, Esq., is the Director of Resolutions at Community Tax LLC, where he leads a team of practitioners and service professionals dedicated to resolving complex tax conflicts, including IRS audits, tax liens, and tax debt. A licensed attorney, tax practitioner, and notary public in Puerto Rico, Markos combines his extensive legal expertise and management skills to deliver exceptional results and reduce stress for his clients. He holds a Juris Doctor from the University of Puerto Rico School of Law and has experience in a variety of legal fields, as well as industrial management. Bilingual in English and Spanish, Markos is also a published researcher with a passion for delivering outstanding service.