You and Your Form W2: What It Says, Why You Need It, and Where You Can Get Last Year’s W2

Published:How do you do that Form W2 voodoo you do so well?

One of the most important documents for filing your federal income taxes is the Wage and Tax Statement Form, also known as Internal Revenue Service W2 Form.

It’s the bread and butter of most taxpayer’s federal returns. Because, like most taxpayers, you earn your living from an employer.

So, what happens if you have employer issues?

What exactly does the Form W2 Wage and Tax Statement say about you and your employer?

What if you’re missing employment tax records for a few years and need proof of income for some reason?

What Exactly Is a W2 Form?

Tax form W2 is a document that employers are required to send to employees and the IRS. It contains your wage and salary information, as well as the taxes withheld from your paychecks for Social Security-related reasons. These withholding taxes (also known as ‘payroll withholding’) are sent directly to the IRS by your employer. They act like a credit towards the income taxes that you must pay for the year. The W-2 form also reports Social Security tax, a.k.a. the Federal Insurance Contributions Act (FICA) tax, to the Social Security Administration.

Who Must File a W2 Form?

Employers are required to file Form W-2 for each employee. They must report the wages that are paid to each employee from whom:

- Income, Social Security, or Medicare Tax was withheld; OR

- Income that tax would have been withheld (if the employee had claimed no more than one withholding allowance, or had not claimed exemption from withholding on their Form W-4)

Additionally, every employer who is engaged in a business that pays remuneration for services performed by an employee (including non-cash payments) must file a Form W-2 for each employee — even if the employee is related to the employer.

It’s important to note that employers do not fill out w-2 forms for self-employed workers or contractors. These workers work for themselves, so they are responsible for making their own estimated tax payments. If you are an employer who used the services of an independent contractor, you are responsible for filling out form 1099-NEC to report the compensation paid to that contractor.

When are -2 forms due?

The W2 Form is the responsibility of the employer. You just get paper copies. Providing you with an up-to-date Form W-2 is an employer obligation, usually something the payroll provider or the team in charge of financial records at your company would do.

Employers are required to complete a W-2 Form for each of their employees, and they must deliver it to each employee by January 31st of the calendar year. W2 Forms will report all the wages and taxes of the employees of that business for the prior calendar year.

Employers must then file the W-2 Forms along with W-3 forms for each employee with the Social Security Administration (SSA) by the last day of February (if filing by paper mail) or the last day of March (if filing electronically). The SSA uses the information on these forms to calculate the Social Security benefits to which each worker is entitled.

What does the W-2 form tell you?

The W-2 form includes important information that you need to file personal tax returns. It reports:

- total wages

- federal, state, and local taxes withheld

- tips

- contributions to retirement plans, like a 401(k)

- contributions to a health savings account

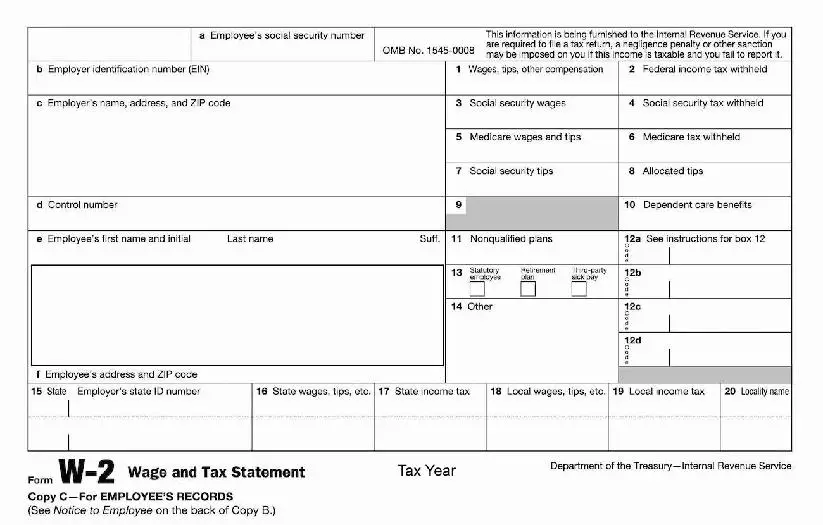

All of this information is displayed in the numbered boxes on the W-2 form. The W-2 form example and bullet points below show how to read a W-2 form:

You can also see a full W-2 form example by clicking here.

- Boxes A-F cover employer and employee identification information.

- Box 1 shows the total taxable compensation that the employee was paid throughout the year. This includes wages, tips, bonuses, and life insurance benefits.

- Box 2 shows the income taxes withheld from the employee’s paychecks throughout the year. As noted, these withholdings work as a credit towards an employee’s income taxes. If you are an employee, you will be able to determine how much is withheld from your paycheck by completing a W-4 form for your employer.

- Box 3-6: Box 3 and 5 show the amount of wages that are subject to the Social Security and Medicare taxes. These figures may be different from the total taxable compensation listed in Box 1. Box 4 and 6 show how much money was withheld for each tax.

- Box 7-8: Box 7 shows the amount of tip money an employee has reported to an employer. Box 8 shows any additional tip income the employer has allocated to an employee that wasn’t reported in box 7.

- Box 9 has been grayed out, as the benefit no longer exists.

- Box 10 reports the total amount of dependent care expenses/services (e.g., daycare facilities) that were paid for or provided by the employer.

- Box 11 any amount of deferred compensation from an employer’s non-qualified plan or nongovernmental pension plan.

- Box 12 shows any other types of compensations or reductions to an employee’s taxable income. This includes things like contributions to a 401(k). Each item will have a code composed of a letter followed by a number.

- Box 13 contains three checkboxes. An employer will check these boxes if 1) an employee worked as a statutory employee not subject to federal income tax withholding, 2) the employee participated in an employer-sponsored retirement plan like a 401(k), or 3) the employee received sick pay through a third party, like an insurance policy.

- Box 14 gives an employer space to include any other tax information that didn’t fit into the other boxes.

- Box 15 is the employer’s state ID number.

- Box 16-20 reports the employee’s total taxable income at the state and local level, as well as the amount of taxes withheld for each level of government.

You can find a more detailed explanation of each box here.

If you are an employer, you’ll notice that the W-2 form example above contains 6 copies of the form. This is because the form needs to be sent to several different government offices and the employee. For a full explanation of the purpose of each copy, click here.

Why You Need IRS Form W-2

If you’re an employee, you need your W-2 in order to file an accurate income tax return (Form 1040) with the IRS. When preparing your annual return, you will use your W-2 form to report your earnings and any taxes withheld from that income. If you had more than one employer during the year, you will use multiple W-2 forms to complete your taxes.

Employers are required to provide W-2s to their employees by the end of January every year. (For example, you should receive your 2022 W-2 by January 31, 2023.) You may be given your W-2 in person at work, or you might receive it by mail – in which case you should be on the lookout around this time. Remember that it is important to retain copies of your tax returns and any supporting documents.

How to Replace a Missing or Lost W-2

First, don’t panic! Many people go through this each year. If you don’t have your W-2 by mid-February, here’s what you can do:

Contact Your Employer

The first course of action should be to ask your employer directly for a copy of your W-2 form – the human resources or payroll department usually handles this type of paperwork. If they can mail it to you, make sure they have the correct mailing address.

Contact the IRS

While it’s frustrating, you still have some options even if you don’t get your W-2 from your employer.

If you get no response from your employer by February 14, you can call the IRS for support (1-800-829-1040). The IRS will reach out to your employer on your behalf, which may help motivate them to respond. You’ll need to provide information to the IRS when you call, including:

- Your name, street address, city, state, ZIP code, Social Security Number (SSN), and phone number

- Your employer’s name, address, and phone number

- The dates you were employed

- An estimate of your wages and any federal income tax withheld for the year – this should be based on your last pay stub, or Leave and Earnings Statement (LES) for federal employees, if you have it

File Your Tax Return On Time

Remember that you have until April 15 to file your taxes (or request a tax extension) whether or not you receive your W-2. Therefore, you should still plan on filing and paying your taxes by the original due date.

File a Substitute W-2 (Form 4852)

If you’ve exhausted the above options and still haven’t received your W-2, you can use Form 4852 (Substitute for Form W-2, Wage and Tax Statement). You will need to estimate your income and federal tax withheld – as close to accurate as you can – and attach Form 4852 to your tax return. Keep in mind that there might be a delay in processing your tax refund while the IRS verifies your information.

File a Tax Extension

If you don’t think you’ll have your Form W-2 by the filing deadline and you don’t want to use a substitute form, you can apply for a tax extension to avoid IRS late fees and penalties. An extension will give you 6 extra months to file your return, however, it does not give you more time to pay your tax balance. You will need to file an extension application (Form 4868) and pay any tax due by the original deadline (April 15). You can easily request an extension online and pay your taxes at the same time.

File an Amended Return (Form 1040X)

If you decide to file your tax return using Form 4852 as a substitute and then you receive your actual Form W-2 after you’ve filed, you will need to compare them. If the information on your actual W-2 is different from what you reported with Form 4852, you will need to correct your return. You should do this by filing Form 1040X (Amended U.S. Individual Income Tax Return) with the IRS.

Order a Transcript or Copy of Your Form W-2

Do you need a copy of your W-2 from the previous year? You can get a transcript of your reported income from the IRS, but an actual copy of your W-2 can only be obtained if you submitted it with a paper tax return (Form 1040).

Wage and Income Transcript

This transcript shows the federal tax information that your employer reported to the Social Security Administration. It contains data from information returns that the IRS receives, including Forms W-2, 1098, 1099, and 5498. It’s available for up to 10 prior years, though current tax year data may not be ready until July. Want to see how much you made 10 years ago? Ask for a wage and income tax transcript. You can do it through the online portal Get Transcript tool from the Internal Revenue Service. If you like postage and waiting, you can also submit Form 4506-T (Request for Transcript of Tax Return).

Previous Employer Not Available? Ask the IRS for a Copy

Can’t get a copy of your W-2 from your previous employer? If you submitted an actual W-2 form on a paper return, you can get one from the IRS. Just ask for a copy of your entire return from the year you need, and the W-2 will be attached. Use Form 4506 (Request for Copy of Tax Return), but note the IRS charges for copies of tax returns. It’s $50 fee per personal tax return.

If you e-file your taxes online or you didn’t submit your W-2 with your 1040 paper return, you can request a transcript from the IRS. Otherwise, you will have to reach out to your employer or contact the SSA for a copy of your W-2 form.

Sources

“How To Use Form W2 for Federal and State Income Tax Returns | Tax Info from IRS.com” – Tax Info

“I lost my Form W-2 What are my Options?” – Jason D. Knott

Related Articles

You May Also Like