The Star of the Show: El Formulario 1040 es el formulario estrella del Servicio de Impuestos Internos (IRS). Se utiliza para reportar los ingresos de un individuo y calcular sus impuestos federales sobre los ingresos. Este formulario lo utilizan todos los ciudadanos y residentes permanentes que están obligados a presentar una declaración de impuestos cada año.

The Many Parts of Form 1040: El formulario 1040 consta de varios anexos, como el anexo E para los ingresos por rentas o el anexo 2 para los impuestos adicionales. Dependiendo de su tipo de ingresos, es posible que tenga que completar determinados anexos al presentar el formulario 1040. Además, las deducciones detalladas y los ajustes a los ingresos pueden reportarse en el formulario 1040.

Fechas límite: Tanto si presenta una declaración digital como en papel, la fecha límite para la presentación de las declaraciones de impuestos de los individuos suele ser el 15 de abril de cada año. Sin embargo, si no puede presentarla antes de esa fecha, puede solicitar una prórroga o presentar una declaración enmendada más adelante en el año.

Form 1040 is the Main Tax Form for Individuals: If you're filing a personal income tax return, Form 1040 is the form you need to use. 1040 is the go-to form for reporting income, claiming deductions, and figuring out your tax liability (or how much you'll get as a refund).

The Instructions Explain Every Section: Unsure of what to do? The IRS provides detailed instructions to help you complete Form 1040. These include explanations for each line, who needs to file, tax brackets, and how to handle things like credits and deductions.

Standard Deduction vs. Itemizing: The instructions walk you through whether you should take the standard deduction or itemize your deductions. The standard deduction is easier, but itemizing could save you more money if you have significant deductible expenses (like mortgage interest or medical bills).

Schedules May Be Required: Some taxpayers need to attach additional forms called schedules. For example, Schedule 1 reports extra income (like unemployment or self-employment income), while Schedule 3 includes certain tax credits. The instructions explain which schedules you need.

Electronic Filing is Encouraged: To the surprise of no one, the IRS prefers electronic filing (e-file) since it's faster (both for you and them), more secure, and reduces errors. The instructions provide guidance on e-filing, payment options, and direct deposit for refunds.

There are a lot of these Form 1040 pages! However, it’s the main form for everyone’s tax return, from Bond villains to Disney princesses. So while it seems a little daunting at first, don’t worry about getting stuck; after all, its in the IRS’s best interest that pretty much every taxpayer is able to find their way around this Form to file (and pay) their taxes.

El Formulario 1040 es el formulario estrella del Servicio de Impuestos Internos (IRS). Se utiliza para reportar los ingresos de un individuo y calcular sus impuestos federales sobre los ingresos. Este formulario lo utilizan todos los ciudadanos y residentes permanentes que están obligados a presentar una declaración de impuestos cada año.

Form 1040 consists of several schedules, such as Schedule E for rental income or Schedule 2 for additional taxes. Depending on your type of income, you may need to complete certain schedules, so this Form 1040 instructions will be of great help to you. Additionally, itemized deductions and adjustments to income can be reported on it.

Tanto si presenta una declaración digital como en papel, la fecha límite para la presentación de las declaraciones de impuestos de los individuos suele ser el 15 de abril de cada año. Sin embargo, si no puede presentarla antes de esa fecha, puede solicitar una prórroga o presentar una declaración enmendada más adelante en el año.

Todos los tipos de formularios de declaración de impuestos sobre los ingresos de los individuos en Estados Unidos

Normalmente, tendría que presentar formularios adicionales para su situación fiscal particular y le permite reclamar los ingresos, las deducciones estándar, los créditos, etc. que le correspondan.

¿Sabía que existen muchos tipos diferentes de formularios de declaración de impuestos sobre los ingresos de los individuos?

Los tipos más comunes de formularios de declaración de impuestos sobre los ingresos son los siguientes:

Formulario 1040 (Declaración del impuesto sobre los ingresos de los individuos en Estados Unidos) (también conocido como "el formulario largo").

Formulario 1040A (Declaración de impuestos sobre los ingresos de los individuos en Estados Unidos) (también conocido como "el formulario corto").

Formulario 1040EZ (Declaración de impuestos sobre los ingresos de extranjeros no residentes en Estados Unidos).

Formulario 1040NR (Declaración de la renta de los extranjeros no residentes en EE.UU.)

Formulario 1040NR-EZ (Declaración de impuestos sobre los ingresos de EE.UU. para determinados extranjeros no residentes sin personas a su cargo).

The U.S. Individual Income Tax Return Form Everyone Knows: IRS Tax Form 1040 Instructions

Form 1040 is the standard federal income tax form used to report an individual’s gross taxable income (e.g., money, goods, property, and services) as well as the additional schedules for deductions beyond the standard deduction. It is also known as “the long form” because it is more extensive than the shorter 1040A and 1040EZ Tax Forms.

Most tax forms focus on a single deduction or tax credit or income source. IRS Form 1040 lets individual taxpayers to claim expenses andcréditos fiscales, reportar ingresos gravables y no gravables,detallar deducciones, e incluso reportarimpuestos sobre ganancias de capital, todo en el mismo formulario. Aunque el formulario de la declaración de impuestos sobre los ingresos de los individuos de Estados Unidos puede tardar más en completarse, es su principal

Por lo general, el Formulario 1040 debe presentarse antes del 15 de abril, a menos que solicite una extensión fiscal automática. Si no presenta su declaración de impuestos sobre los ingresos personales antes de esta fecha, estará sujeto a penalizaciones y/o cuotas por retraso. Puede solicitar una extensión de impuestos presentando el Formulario 4868 del IRS antes de la fecha límite de presentación (15 de abril).

Hay muchas formas diferentes de obtener el Formulario 1040 de impuestos. La opción más rápida y cómoda es descargar el formulario de impuestos en su computadora. Además, la mayoría de las oficinas de correos y las bibliotecas locales tienen formularios de impuestos durante la temporada de presentación, y los formularios también se pueden recoger en un centro de impuestos o en una oficina del IRS.

¿Qué formularios en papel e información necesita para el Formulario 1040?

Antes de empezar a presentar su declaración anual de impuestos sobre los ingresos, asegúrese de tener preparada la siguiente información:

Remember that annual tax return, with payment, is due by April 15th. The Internal Revenue Service may grant a 6-month tax extension for your federal income tax return (with IRS Tax Form 4868) for late filing, but payments must still be made by April 15.

You may file your federal tax forms by paper mail, by using IRS e-file, or through an approvedpreparador de impuestos autorizado. La presentación en papel es siempre la más lenta para obtener cualquier reembolso federal o notificación al IRS.

La declaración de impuestos is generally safer, faster, and easier, and you will get your tax refund much sooner if you choose the direct deposit option.

While there are several tax forms to choose from when filing yourimpuestos federales sobre los ingresos, una apuesta segura es utilizar el Formulario 1040 del IRS si no está seguro de si califica o no para el 1040A o el 1040EZ. Las reglas básicas son: En caso de duda, presente el Formulario 1040 del IRS.

De clic AQUÍ para empezar a presentar su Formulario 1040 en línea.

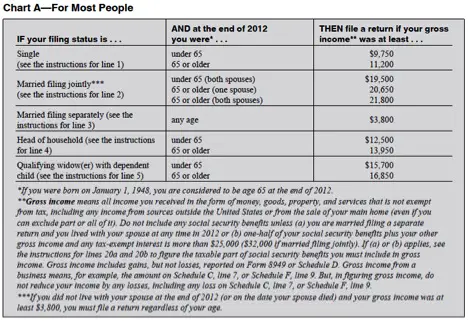

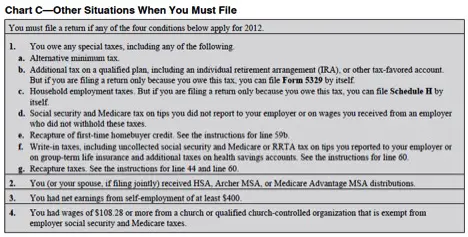

Debe presentar el Formulario 1040 junto con su declaración de impuestos federales si se da alguno de los siguientes casos:

Tiene ingresos gravables de $100,000 o más.

Tiene ingresos de trabajadores independientes de $400 o más.

Le retuvieron el impuesto sobre los ingresos de los cheques de pago.

Hizo pagos de impuestos estimados, o tiene pagos en exceso que se aplican al año fiscal actual.

Tiene deducciones desglosadas (por ejemplo, hipoteca, intereses o caridad).

Obtiene ingresos de un negocio, corporación S, sociedad, fideicomiso, alquiler o granja.

Tiene distribuciones de ganancias de capital procedentes de acciones, bonos o fondos de inversión o de la venta de propiedades.

Reclama ajustes de ingresos (por colegiatura, gastos de educador, gastos de mudanza o cuentas de ahorro para la salud).

Ha recibido un anticipo del Crédito Fiscal por Ingresos Ganados (EITC) de un empleador.

Tiene un Formulario W-2 que muestra impuestos no cobrados (de propinas o seguros de vida colectivos a plazo), o un W-2 que muestra un código Z (ingresos ganados de un plan de compensación diferida no cualificada 409A).

Debe impuestos sobre la remuneración de acciones con información privilegiada.

Es usted deudor en un caso de bancarrota del capítulo 11 (presentado después del 16 de octubre de 2005).

Usted gana ingresos adicionales salarios extranjeros, pagó impuestos extranjeros, o está reclamando beneficios de tratados fiscales.

Debe cualquier otro impuesto especial (por ejemplo, impuesto mínimo alternativo, impuestos sobre el empleo doméstico, impuestos de recuperación, etc.).

Seguro Social y otras prestaciones de jubilaciónSeguro Social y otras prestaciones de jubilación

Al completar el Formulario 1040, es importante reportar todas las prestaciones del Seguro Social que recibió durante el año. Estos ingresos se reportan en la línea "Prestaciones del Seguro Social" del Formulario 1040 y deben incluirse al calcular sus ingresos gravables totales. Si recibe prestaciones de jubilación ferroviaria, también deberá reportarlas al mismo tiempo.

Otros tipos de ingresos gravables procedentes de fuentes que incluyen los ingresos empresariales

There are many other types of income that must be reported on Form 1040. This includes any wages, salaries, or tips earned during the year. Any commissions, bonuses, or other forms of compensation should also be included. Self-employment income from freelancing or running a business must also be reported, as well as any interest or dividends earned from investments.

If you received any royalties for the use of property such as copyrights or patents, then these amounts should also be reported. Finally, rental income should also be included if you own rental properties and receive payment for them.

Deducciones y créditos aplicables al Formulario 1040

Deductions and credits can be used to reduce your taxable income when filing Form 1040. Common deductions include charitable contributions, student loan interest, health savings account contributions, and self-employment expenses.

Additionally, you may qualify for certain tax credits, such as the Child Tax Credit and the Earned Income Tax Credit. The rules for these deductions and credits vary from year to year, so it is important to stay up-to-date with relevant IRS publications.

Deducción estándar vs. deducciones desglosadas

Standard deductions and itemized deductions are two types of deductions available to taxpayers when filing Form 1040. The standard deduction is a fixed amount set by the IRS and generally applies to most taxpayers who do not itemize their deductions.

On the other hand, itemizing allows taxpayers to deduct certain expenses that exceed the threshold established by the IRS. Common expenses that can be deducted include medical costs, state taxes, mortgage interest, and charitable contributions.

IRS Form 1040 Instructions: FAQ

1. What is IRS Form 1040, and why do I need it?

IRS Form 1040 is the main tax form used by U.S. taxpayers to report their income and determine how much they owe (or get refunded). If you earn income, you’ll likely need to file a 1040 to report wages, deductions, credits, and any taxes paid throughout the year.

2. Where can I find IRS Form 1040 instructions?

You can find the official IRS Form 1040 instructions on the IRS website (IRS.gov). They provide a step-by-step guide on how to fill out the form, explain tax brackets, and outline deductions and credits you might qualify for.

3. What are the main sections of Form 1040?

Form 1040 includes sections for personal info, income sources (like wages, dividends, or self-employment income), tax deductions and credits, and finally, the total tax owed or refund due. The instructions help you figure out which sections apply to you.

4. What’s the difference between a 1040, 1040-SR, and 1040-NR?

1040: The standard form for most taxpayers.

1040-SR: A simplified version for seniors (age 65+), with larger text and a more straightforward layout.

1040-NR: For non-U.S. residents who need to file taxes on income earned in the U.S.

5. Do I need to attach other forms to my 1040?

Well, it depends! If you’re claiming deductions (like student loan interest or business expenses) or reporting extra income (from freelancing or investments), you may need to attach additional schedules or forms. The 1040 instructions tell you which ones to include.

6. Can I file my 1040 online or do I have to mail it?

You can do either! The IRS allows electronic filing (e-filing) through tax software or authorized providers, which is faster and reduces errors. If you prefer, you can still print and mail a paper copy to the IRS, but it may take longer to process.

Jacob Dayan is the CEO and co-founder of Community Tax LLC, a leading tax resolution company known for its exceptional customer service and industry recognition. With a Bachelor’s degree in Business Administration from the University of Michigan’s Ross School of Business, Jacob began his career as a financial analyst and trader at Bear Stearns and Millennium Partners before transitioning to entrepreneurship. Since 2010, he has led Community Tax, assembling a team of skilled attorneys, CPAs, and enrolled agents to assist individuals and businesses with tax resolution, preparation, bookkeeping, and accounting. A licensed attorney in Illinois and Magna Cum Laude graduate of Mitchell Hamline School of Law, Jacob is dedicated to helping clients navigate complex financial and legal challenges.